Automotive dealers: Filling the service gap

Last month I stuck my neck out and gave my forecast for the automotive sector this year. It drew a lot more interest than I expected.

The theme that a number of you got in touch about was the scale of the service gap due to reduced new sales. This month I’m going to focus on this in more depth.

So what is the scale of the service gap? Bear with me because I’m going to get somewhat detailed and technical, but if you can follow my reasoning I’ll give you a graphic example of the challenge.

Due to Covid we’ve seen a significant decline in new car sales for the last two years. There’s no sign that this will change in 2022 due to the shortage of chips. Combine this with the fact the franchise dealers see a reduction in the service work as vehicles get older. It’s easy to see that this will affect the amount of service work going forward.

Finally, as electric vehicles require cheaper and less frequent servicing, their growth will eat into the available service parc.

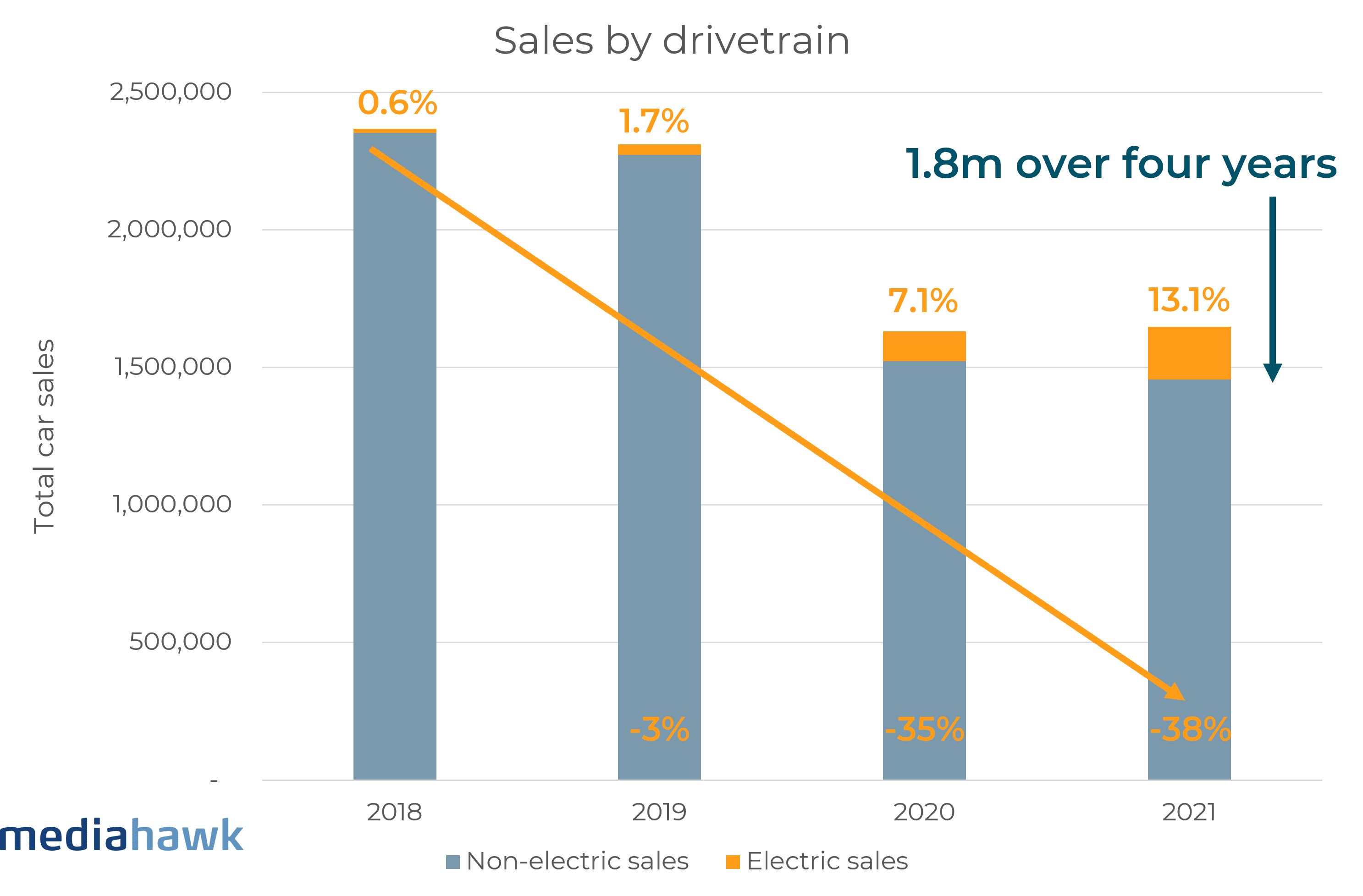

To understand the scale of this, we can model the overall difference of sales from 2018 if they had stayed constant compared to what has actually happened. By removing electric sales during this period from the mix, then we estimate the overall reduction in vehicles that franchise dealers would service is circa 1.8 million vehicles – or a 19% decline – in what would have been expected.

Interestingly in 2021, pure electric vehicles now represent 13.1% of all car sales, compared with only 8% for pure diesel. This can be graphed as follows:

Applying this logic, the top 10 automotive brands with the greatest percentage decline in their sales since 2018 are as follows:

| Brand | 2018 constant sales |

2018 – 2022 actual sales |

Difference | % change |

|---|---|---|---|---|

| Smart | 30,524 | 14,611 | -15,913 | -52% |

| Abarth | 22,524 | 13,763 | -8,761 | -39% |

| Alfa Romeo | 16,644 | 11,255 | -5,389 | -32% |

| Maserati | 5,188 | 3,580 | -1,608 | -31% |

| DS | 20,296 | 14,114 | -6,182 | -30% |

| SsangYong | 11,016 | 7,697 | -3,319 | -30% |

| Honda | 210,280 | 150,708 | -59,572 | -28% |

| Subaru | 12,564 | 9,196 | -3,368 | -27% |

| Fiat | 142,608 | 104,949 | -37,659 | -26% |

| Vauxhall | 709,192 | 524,024 | -185,168 | -26% |

| Total | 1,180,836 | 853,897 | -326,939 | -28% |

The top five winners since 2018 are:

| Brand | 2018 constant sales |

2018 – 2022 actual sales |

Difference | % change |

|---|---|---|---|---|

| Tesla | 19,168 | 81,860 | 62,692 | 327% |

| MG | 36,196 | 71,139 | 34,943 | 97% |

| Lexus | 49,620 | 55,723 | 6,103 | 12% |

| Porsche | 49,748 | 55,680 | 5,932 | 12% |

| Volvo | 201,276 | 201,195 | -81 | 0% |

| Total | 356,008 | 465,597 | 109,589 | 31% |

If you’re a franchise dealer, it’s critical that you understand the scale of the service gap for the brand(s) you represent. I’m happy to provide this data if you get in touch.

Headline Autotrader figures

Due to the tightness of the market, Autotrader have yet to show any stock for 2022 plate.

- 2021 stock, MoM 41% increase, YoY 49.6% decrease

- 2020 stock MoM 1.5% decrease, YoY 40.9% decrease

- Total market MoM no change, YoY 15.3% decrease

Top 5 brands by market share of 2021 stock

- VW 11.6%

- BMW 10.5%

- Audi 10.1%

- Mercedes 6.0%

- Ford 5.9%

Get in touch if you want more of my research across all the automotive brands for the service gap. Furthermore, I’ve been working with a number of my customers on the appropriate marketing activity to tackle the issue, and am happy to give you some ideas in this area.